Lease Accounting Software for IFRS 16 & FRS 102,

Simplified.

The effortless way to manage your lease accounting under FRS 102.

AI-driven extraction, audit-ready schedules, zero headaches.

Why Spreadsheets Break

Under FRS 102 Lease Accounting

Finance teams waste hundreds of hours patching formulas that lack the design for lease accounting.

Complex Calculations

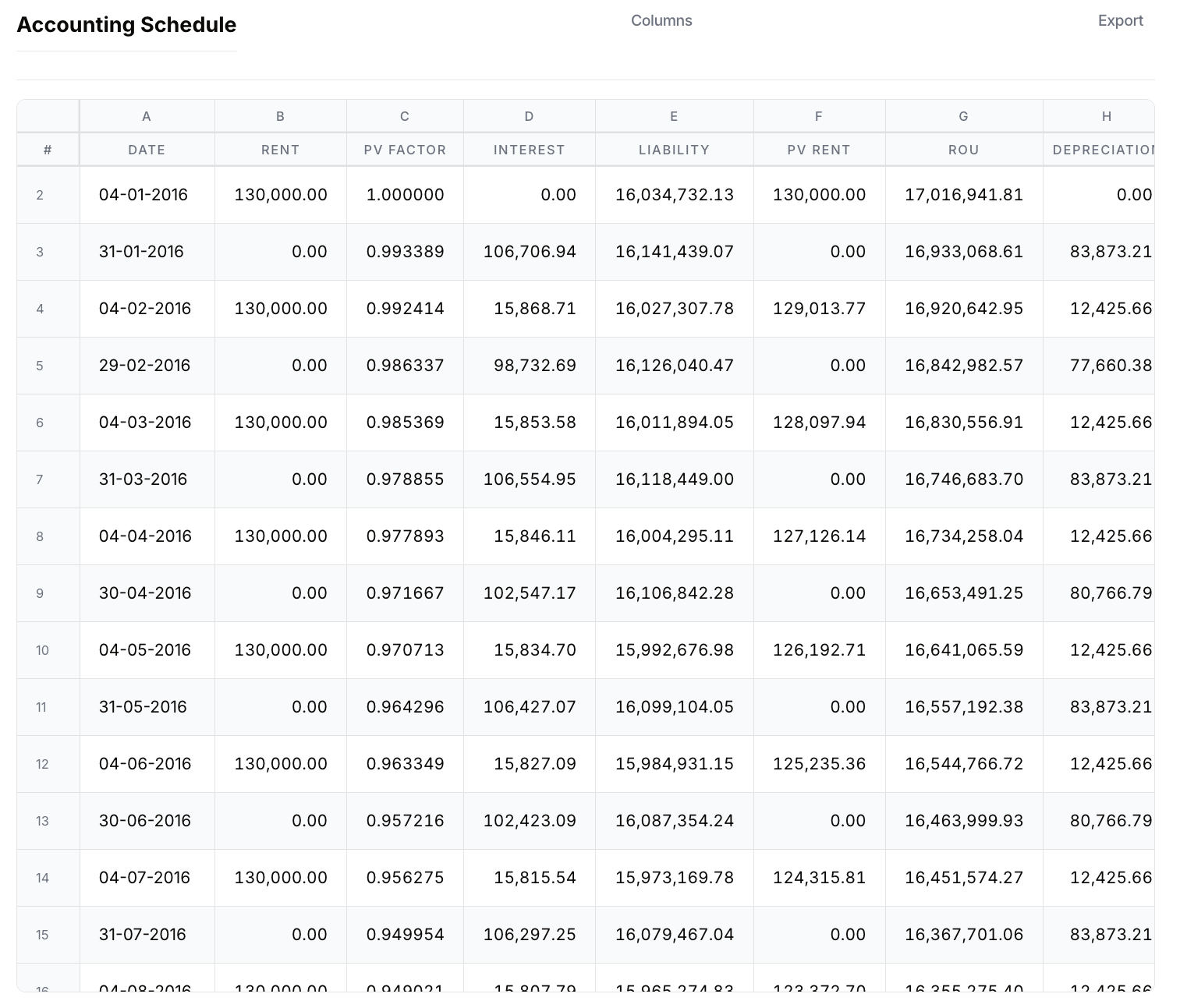

Right-of-use assets, discounted lease liabilities, and effective-interest amortisation in lease accounting are too complex for any manual formula chain. One error cascades through every period.

No Audit Trail for Lease Accounting

Auditors can't trace overwritten cells. Spreadsheets have no version history, no user attribution, and no formula lock — leaving you exposed at year-end.

Modification Complexity

A single lease extension or indexation change requires recalculating every downstream period. In a spreadsheet, this takes days and introduces fresh risk every time.

Journal Generation

Producing FRS 102-compliant journals for initial recognition, monthly charges, and modifications requires discipline and deep standard knowledge. Do not rely on copy-paste.

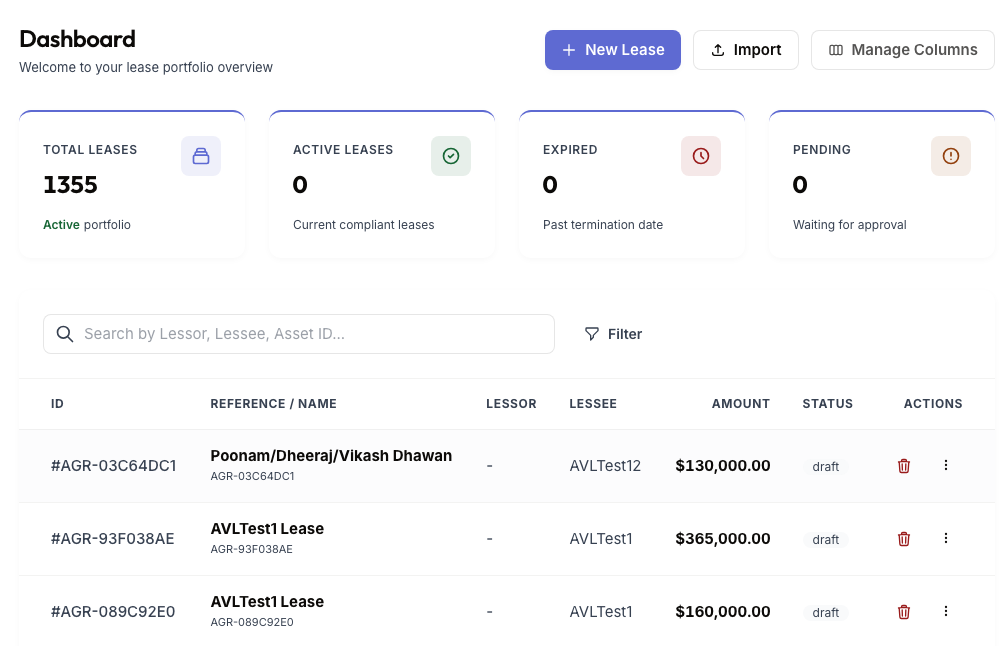

From Upload to Compliant Close

Four steps. No consultants. No months of implementation.

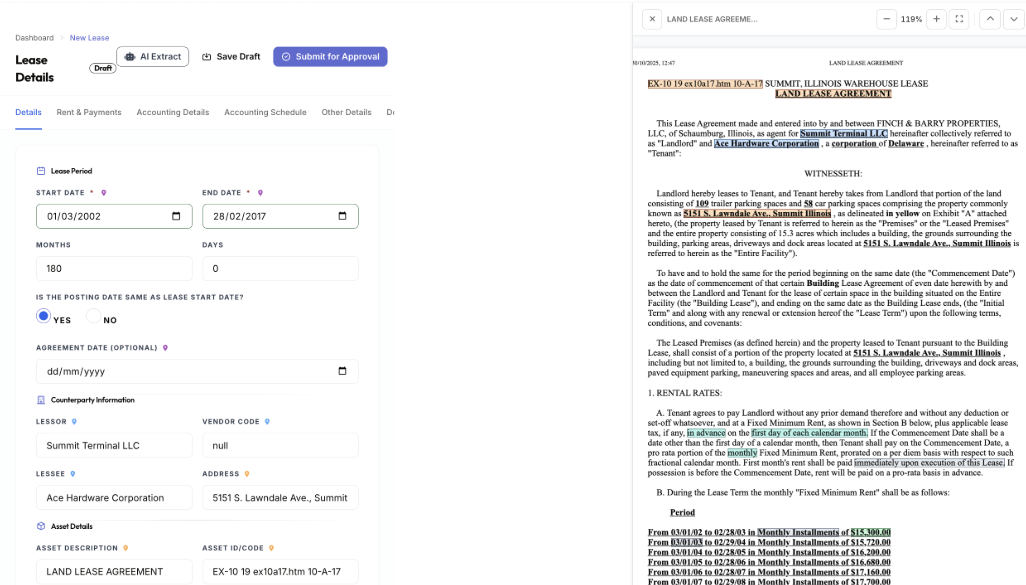

Upload

Drop your lease contracts. QuantLease lease accounting software accepts any format and handles any volume.

Extract

AI reads every clause and extracts key fields with confidence scores. You review, correct, confirm — done.

Calculate

Full amortisation schedules, ROU asset values, and interest charges computed instantly — to the penny, every period.

Report

Export audit-ready journals, FRS 102 disclosure notes, and Excel schedules. Close your books with confidence.

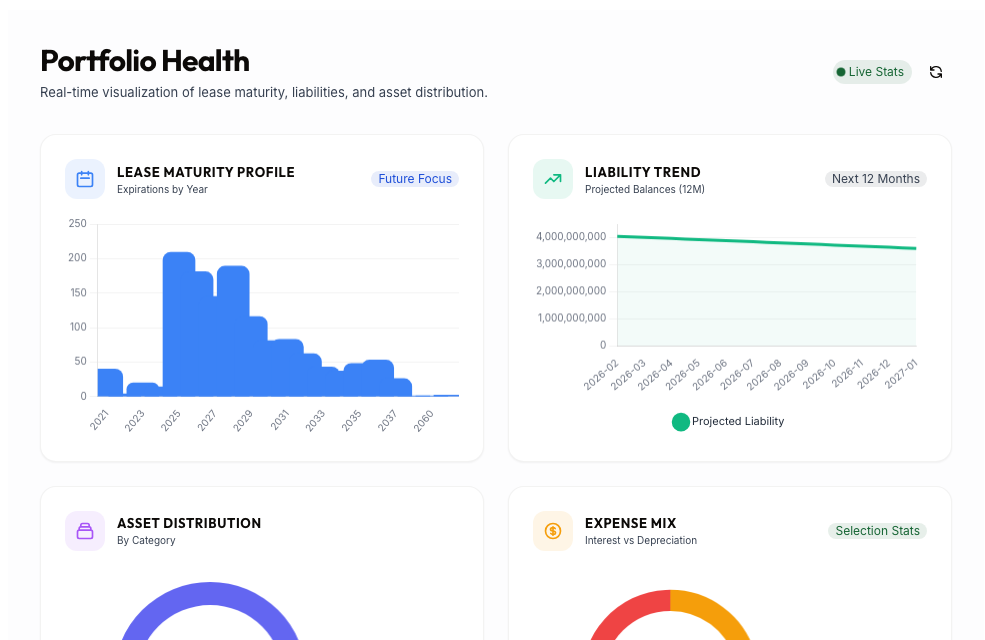

Lease Accounting Built for the entire Finance Ecosystem.

QuantLease delivers the specific workflow, controls, and data each role demands. Whether you are closing the books, signing them off, or auditing them, we have you covered.

Month-End Close · ERP Sync · Journal Precision

- Month-End Close Acceleration: Pre-calculated amortisation and interest postings are ready to export on day one. This cuts close time by up to 80%.

- ERP Synchronisation: Get native journal import formats for Sage 50, Sage Intacct, Xero, and NetSuite. We map these directly to your internal chart of accounts at go-live.

- Journal Entry Precision: Every posting computed via the effective interest method at the correct periodic rate — no formula skill required.

QuantLease vs Spreadsheets

Everything you need for FRS 102 lease accounting compliance — and nothing spreadsheets can deliver.

| Capability | QuantLease | Spreadsheet |

|---|---|---|

| FRS 102 Calculation Engine | ✓ Automated, always correct | ✗ Manual, error-prone |

| AI Document Extraction | ✓ Upload & extract in minutes | ✗ Manual data entry only |

| Audit Trail & Version History | ✓ Every change attributed & logged | ✗ No traceability |

| Lease Modifications & Remeasurement | ✓ Instant recalculation | ✗ Days of manual rework |

| Journal Entry Generation | ✓ FRS 102-compliant, ERP-ready | ✗ Written manually each period |

| Disclosure Note Reports | ✓ One-click PDF generation | ✗ Built from scratch annually |

| Multi-user & Role-Based Access | ✓ RBAC with SSO support | ✗ Shared file, no controls |

| Amortisation Schedule Export | ✓ Excel with embedded formulas | ~ Manual, formula-free |

| Disaster Recovery | ✓ Automated cloud backups, 99.9% SLA | ✗ Local file risk — single point of failure |

| Accounting Standard Updates | ✓ Automatic — 2026 FRS 102 ready | ✗ Manual formula rewrites required |

Tailored for your

Organisation.

Custom integrations, dedicated support, on-premise deployment options, and an SLA you can rely on. Built for finance teams that can't afford downtime.

Latest from the Knowledge Center

Lease Accounting Under IFRS 16 and FRS 102: A Practical Guide

Everything finance leaders need to know about ROU asset calculation and the FRS 102 2026 amendments.

Read Article → Corporate RiskWhy Excel is the Biggest Risk to Your IFRS 16 Compliance

Spreadsheet dependency is the leading cause of audit failures in lease accounting.

Read Article → GovernanceThe Auditor's Year-End IFRS 16 Checklist

Is your lease portfolio ready for clinical auditor scrutiny at year-end?

Read Article → Technical DepthIFRS 16 Day 2 Lease Modifications: The Complete Accounting Guide

How to handle post-transition lease modifications, reassessments, and IBR updates without audit risk.

Read Article → TransitionIFRS 16 Transition Approaches: Full vs Modified Retrospective

Choose the right transition method for your first FRS 102 or IFRS 16 reporting period and avoid restatement shocks.

Read Article →Lease Accounting Glossary

Click any term to expand the definition.

A cloud or IT arrangement only falls under lease accounting if the customer controls a specific, identifiable asset throughout the contract term. Where a supplier retains substantive substitution rights, the arrangement is a service contract — not a lease.

- Key test: Does the customer control the identified asset? If yes → ROU asset required.

The IBR is the rate a lessee would pay to borrow a similar amount over a similar term — and it is the most audited input in any lease accounting file. It must be set individually per lease at commencement, not as a blanket portfolio rate.

- QuantLease IBR Register documents rate, benchmark, methodology, and approving signatory for every lease.

The commencement date — when the asset is made available — is when the accounting clock starts. It is distinct from the contract inception date and is frequently later, especially for pre-let property agreements.

- Common error: Using the contract signing date instead of the asset availability date shifts interest and depreciation to the wrong periods.

Both IFRS 16 and FRS 102 Section 20 allow optional simplifications: leases of 12 months or less (short-term exemption) and assets worth ≤ USD 5,000 when new (low-value exemption) may be expensed straight-line instead of being capitalised.

- Caution: Short-term elections apply per asset class, not per lease — and require an explicit accounting policy note.

You can expense assets qualifying as low-value (laptops, phones, small office equipment) on a straight-line basis regardless of term. Unlike the short-term exemption, you must make this assessment lease-by-lease, not on a class basis.

- Does not apply to sub-leased assets or high-value assets on a low payment schedule.

When a rent review clause links payments to CPI or RPI, each review date triggers a remeasurement — not on every index movement. You discount the revised liability at the current IBR, with the adjustment posted to the ROU asset, not P&L.

- QuantLease tracks review dates, flags remeasurements automatically, and regenerates all affected schedules.

An ROU asset represents a lessee's right to use an underlying asset for the lease term. You initially measure it at the same amount as the lease liability, adjusted for any lease incentives received, initial direct costs, and prepaid or accrued lease payments.

- Depreciation: Straight-line over the shorter of the lease term and the asset's useful life — unless ownership transfers at end of term.

The lease liability is the present value of all future lease payments not yet made, discounted at the IBR (or the implicit rate if determinable). It unwinds each period via the effective interest method — increasing by interest accrual and reducing by cash payments.

- Balance sheet split: Current (due within 12 months) and non-current — both must be disclosed separately.

Under old UK GAAP, leases were classified as finance (on-balance-sheet) or operating (off-balance-sheet). IFRS 16 and the FRS 102 2026 amendments eliminate this distinction for lessees — all qualifying leases are now capitalised.

- Note: The finance/operating distinction is retained for lessors under both IFRS 16 and FRS 102.

A sale and leaseback occurs when an entity sells an asset and simultaneously leases it back from the buyer. Under IFRS 16, if the transfer qualifies as a sale, the seller-lessee recognises only a partial gain or loss — limited to the rights transferred to the buyer.

- Key test: Does the transfer meet IFRS 15 / FRS 102 Section 23 criteria to be accounted for as a sale?

A lease modification is any change to the scope or consideration of a lease not in the original terms. Modifications are either treated as a new separate lease or a remeasurement of the existing liability at a revised IBR.

- Common triggers: Exercising an extension option, rent renegotiation, or adding / removing leased space.

Variable lease payments fall into two categories: those that depend on an index or rate (included in the lease liability) and those that depend on performance or usage (excluded and expensed as incurred).

- Example: Turnover-linked rent is excluded; RPI-linked rent is included and remeasured at each review date.

Get Started with QuantLease

Request a demo or start your free trial. We'll get back to you within 24 hours.

Ready to modernise your

lease accounting?

Join forward-thinking finance teams today.

Start Free Trial